Does Insurance Cover Hail Damage in Texas? What Homeowners Need to Know

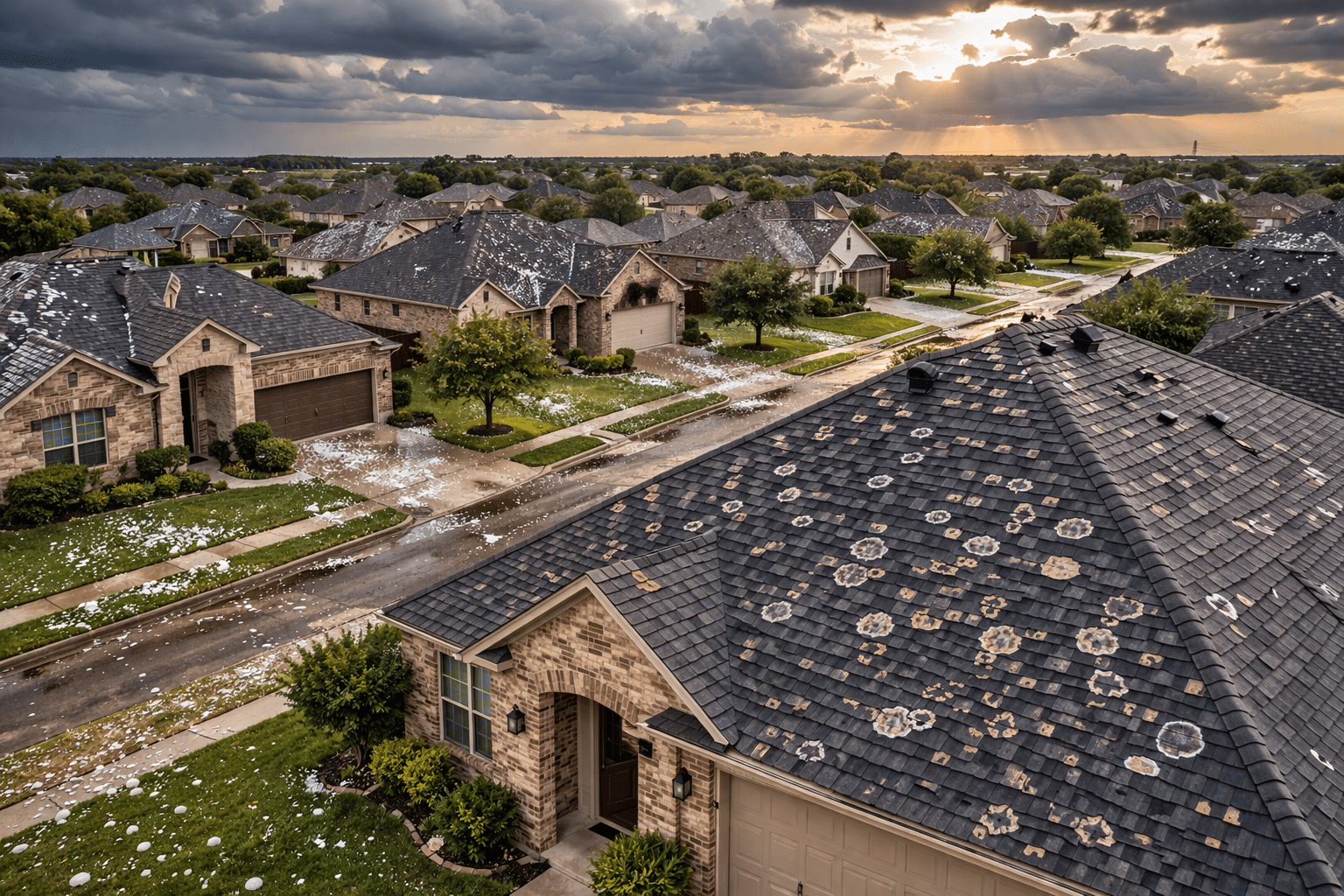

Texas leads the nation in hail events. In a recent twelve-month period, the state recorded more than 600 significant hail storms. Most of them hit in a band stretching from the Panhandle through DFW and south toward San Antonio — exactly where the most homeowners live.

So the question is reasonable: does your homeowners insurance actually cover hail damage?

The short answer is usually yes. However, what your policy pays — and how much it pays — depends on several factors that most Texas homeowners do not check until after the storm. This post explains each one clearly, so you understand your coverage before you need it.

Hail Is a Named Peril in Most Texas Homeowners Policies

Standard Texas homeowners policies cover windstorm and hail as named perils. This means the policy specifically lists hail as a covered cause of loss. Therefore, if a hail storm damages your roof, siding, windows, or other covered structures, your insurer is obligated to pay a valid claim — subject to your deductible and any policy exclusions.

This coverage is not automatic on every policy type. For example, a dwelling fire policy (DP-1) covers only specific named perils and may not include hail. However, for most standard Texas homeowners policies — HO-3 and similar forms — hail coverage is standard.

The Texas Department of Insurance publishes a homeowners claims guide that outlines what most standard policies cover. If you are not sure what form you have, check your declarations page. The policy form number is listed there.

What Your Hail Deductible Actually Means

Coverage is one thing. What you collect is another. In Texas, most homeowners policies now include a separate wind/hail deductible. This deductible is often expressed as a percentage of your home’s insured value — not a flat dollar amount.

A 2% hail deductible on a $350,000 home means you pay $7,000 before insurance pays anything. That is not a small number. In fact, on a smaller claim, the deductible alone can eliminate your payout entirely.

Example: Adjuster values hail damage at $9,000. Your 2% deductible on a $350,000 home is $7,000. Insurance pays $2,000. You pay $7,000 out of pocket.

If you are not sure what your hail deductible is, check the declarations page of your policy. Look for a line labeled “windstorm and hail” deductible or “named storm deductible.” It may be listed separately from your all-other-perils deductible. For a full explanation of how these work, see our post on what a 2% hail deductible means in Texas.

ACV vs. Replacement Cost: What Your Roof Settlement Will Look Like

Even after clearing your deductible, the type of coverage you have on your roof determines how much you actually receive.

Actual Cash Value (ACV) pays the depreciated value of your damaged property. An older roof is worth less than a new one. So the insurer subtracts depreciation before writing the check.

Replacement Cost Value (RCV) pays the full cost to repair or replace your roof with comparable new materials. It does not subtract for age or wear.

For example, suppose your roof replacement costs $18,000. You have a 15-year-old roof with 75% depreciation applied. Under ACV coverage, the insurer pays $4,500 before your deductible. Under RCV coverage, the insurer pays $18,000 before your deductible.

That gap — $13,500 — can determine whether you can actually fix your roof. Many Texas homeowners discover they have ACV-only coverage on the roof after a storm. In high-hail markets, this is increasingly common. Insurers in North Texas and DFW often limit new policies to ACV-only on the roof, especially for homes over 10 years old.

For a complete breakdown of how this works, see our post on ACV vs. replacement cost on Texas hail claims.

What Hail Damage Is Typically Covered

Standard homeowners policies cover hail damage to the dwelling and attached structures. They also cover other structures on the property, such as a detached garage. Here is what most Texas policies will pay on a valid hail claim:

- Roof damage — the most common hail claim by a wide margin

- Siding and gutters — dents, cracks, and penetrations are covered

- Windows and skylights — broken glass or frame damage

- HVAC equipment — exterior units can take significant hail hits

- Personal property — if hail penetrates the structure and damages contents inside

Vehicles are not covered under your homeowners policy. However, comprehensive auto coverage (not collision) covers hail damage to your car. If a hail storm hit both your house and your car, those are two separate claims with two separate deductibles.

What Hail Policies Commonly Exclude

Coverage is not unlimited. Several exclusions commonly limit or eliminate hail payouts in Texas. These are worth knowing before you file.

Pre-existing damage: If your roof had damage before the storm — from a prior hail event, deferred maintenance, or wear and tear — the insurer will likely argue that some of the damage is not attributable to the current loss. The adjuster will inspect and note existing conditions.

Cosmetic damage exclusions: Some Texas policies now include a cosmetic damage endorsement. This excludes dents, dings, or surface blemishes that do not affect the functional performance of the roof or siding. In other words, the policy covers damage that causes leaks — but not dents that only look bad. This endorsement is legal in Texas and more common than most homeowners realize.

Wear and tear: Standard policies exclude wear and tear as a cause of loss. An old, already-deteriorated roof will face depreciation and may face challenges on coverage if the insurer argues that age — not the storm — is the primary cause of loss.

Maintenance exclusions: Damage resulting from a homeowner’s failure to maintain the property can be excluded. For example, if gutters were never cleared and the weight of debris contributed to damage, the insurer may contest that portion of the claim.

Under Texas Insurance Code Section 542, your insurer must acknowledge receipt of your claim within 15 days and accept or deny it within 15 business days of receiving all requested information. If they need more time, they must tell you — and they get one 15-day extension. The Texas Insurance Code Section 542 prompt payment rules are published online. These are your rights. Know them.

What to Do After a Hail Storm

If your area takes a significant hail storm, act on a clear sequence. Do not wait for a contractor to show up and tell you what you have.

First, document everything before any repairs begin. Walk your property and photograph your roof (from the ground if necessary), gutters, siding, windows, and any outdoor equipment. Note the date and time of the storm.

Second, call your insurer directly to report the claim. Do not let a roofing contractor call on your behalf. The claim is yours. You control it.

Third, be present for the adjuster inspection. Ask the adjuster to walk through their findings with you. Request a written copy of the damage estimate.

Fourth, get an independent estimate from a licensed roofing contractor before you accept any payment. If the estimates differ significantly, you have the right to dispute the insurer’s valuation. Most policies include an appraisal clause that allows each party to appoint an appraiser and resolve the dispute through a neutral umpire.

If your claim is delayed or denied and you believe the insurer is not following Texas law, file a complaint with the Texas Department of Insurance. TDI has authority to investigate claims handling violations.

Frequently Asked Questions

Does homeowners insurance in Texas automatically cover hail?

Most standard Texas homeowners policies (HO-3 form) list windstorm and hail as named covered perils. Therefore, hail damage to your dwelling is typically covered. However, the amount you receive depends on your deductible, your roof’s settlement method (ACV or RCV), and any applicable exclusions such as cosmetic damage endorsements. Not all policy types include hail. Check your declarations page to confirm.

What if my hail claim is less than my deductible?

If the adjuster’s damage estimate does not exceed your hail deductible, you will receive nothing from the insurer. This is common in Texas because percentage-based deductibles are high on large homes. For example, a 2% deductible on a $400,000 home is $8,000. A $6,000 damage estimate means insurance pays zero and you pay the full repair cost out of pocket. In this situation, it may not make sense to file a formal claim — since filing a claim that results in no payment can still affect your claims history.

Can my insurer deny a hail claim in Texas?

Yes. Insurers can deny hail claims for legitimate reasons, including pre-existing damage, a cosmetic damage exclusion, or failure to document a covered loss. However, a denial must be in writing and must state the reason for the denial. Under Texas Insurance Code Section 542, if the insurer does not follow the required timelines for responding to and paying claims, they may owe interest and attorney fees in addition to the claim amount. If you believe a denial is improper, consult an attorney.

What is a cosmetic damage exclusion and does my policy have one?

A cosmetic damage exclusion is a policy endorsement that eliminates coverage for hail damage that affects only the appearance of your roof or siding — dents or dings that do not cause leaks or structural problems. This exclusion is legal in Texas and is increasingly common in high-hail-risk areas. To find out if your policy has this exclusion, look for an endorsement titled “Cosmetic Damage” or “Cosmetic Exclusion” in your policy documents. If you cannot find it, call your agent and ask directly.

What does the Texas Insurance Code say about hail claims timelines?

Under Texas Insurance Code Section 542, your insurer must acknowledge your claim within 15 days, accept or deny it within 15 business days after receiving all documentation, and pay accepted claims within 5 business days of acceptance. These are statutory deadlines — not guidelines. If the insurer misses them without justification, they may owe you interest at 18% per year on the delayed amount, plus reasonable attorney fees. This is the 15-15-5 rule, and it applies to all Texas homeowners insurance claims, including hail.

What should I do if my hail claim is underpaid?

Start by requesting a written breakdown of the adjuster’s valuation, including the depreciation schedule applied to your roof. Then get an independent estimate from a licensed roofing contractor. If the numbers differ significantly, ask your insurer for a re-inspection. Most policies include a formal appraisal clause — each side selects an appraiser, and a neutral umpire resolves disagreements. In addition, the Texas Department of Insurance accepts complaints about claims handling at tdi.texas.gov. If the underpayment is substantial, consult a licensed public adjuster or an attorney.

Does the age of my roof affect my hail coverage?

Roof age directly affects your payout if you have ACV (actual cash value) coverage — the older the roof, the higher the depreciation applied, and the less the insurer pays. Some Texas insurers inspect roofs before issuing or renewing policies, and an older roof may result in higher premiums, an ACV-only endorsement, or a refusal to insure at standard rates.

Want to know what your policy actually covers before the next storm?

David Offutt is a licensed Texas insurance agent with 20 years of experience and the author of Understanding Insurance in Simple English. He can review your current coverage, explain your deductible, and help you understand what you actually have.

Reach out at 817insurance.com

This post is for informational purposes only and does not constitute legal or financial advice. Policy terms vary. Always review your specific policy documents or consult a licensed agent or attorney.